State Of The Industry: Survey Says!

Characterizing the state of the commercial greenhouse industry is a daunting task considering how segmented the industry is.

Some growers supply box stores while others serve independent retailers.

Some specialize in bedding plants while others primarily grow container perennials or flowering potted plants.

And some have facilities that warrant their own zip codes while others produce plants in single greenhouses.

The list of differences between U.S. greenhouse businesses is certainly a long one. At the end of each year, though, we survey growers to find out how the industry is doing as a whole. We ask growers about the year’s sales and their sales expectations for the coming year, as well as questions about opportunities and challenges their businesses are facing.

This year, we also surveyed suppliers of growers (i.e. chemicals, containers, fertilizers, etc.) about their sales, prices and priorities for 2011. Here’s what we learned.

Sales Analysis

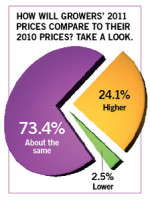

Both growers and their suppliers were asked how their 2010 sales compared to their previous year’s sales. The most popular choice growers selected of the seven options they were presented was “flat.” One in five growers report their 2010 sales were flat compared to 2009.

More growers, however, report sales increases over 2009 (46 percent) than sales decreases (32 percent). In fact, an impressive 18 percent of growers report their overall sales increased more than 10 percent last year. Nearly 14 percent of growers had increases between 5 and 10 percent, and another 14 percent experienced a slight uptick in sales of less than 5 percent.

Last year was even better to growers’ suppliers. Despite a slowly recovering economy, the majority of suppliers indicate their sales were up in 2010 over the previous year. Forty percent, in fact, report sales increases of more than 10 percent.

That 40 percent figure, however, should probably be taken with a grain of salt. Considering the 2009 sales of suppliers, the sales for many had nowhere to go but up.

Still, 73 percent of all suppliers surveyed experienced at least small increases in sales. Thirteen percent of suppliers indicate their sales were flat, and only a few (13 percent) had worse 2010s than 2009s.

In addition to sales, we asked growers how their 2011 production volume will compare to last year’s. Most growers (47 percent) are being fairly bullish, planning to increase their production volume. Thirty-seven percent indicate their production volume will be about the same this year as it was in 2010, and the rest say they’re cutting back some. Only 2 percent say they’ll cut production back more than 10 percent.

Crops & Inputs

We also wanted to get a more precise idea which crops growers are optimistic and pessimistic about for 2011. Like last year, growers are most optimistic about herbs and vegetables. Ornamental bedding plants were also rated highly, and container perennials and flowering potted plants received some support.

Growers are most pessimistic, meanwhile, about trees, woody ornamentals and fresh cut flowers. Many expect the housing market to plague nursery producers again in 2011, and late-2010 announcements such as Carolina Nurseries closing and Monrovia being pressured by its bank to book $20 million in sales by Jan. 31, make more doubters than believers

Beyond crops, we asked growers about the inputs putting the biggest burdens on their businesses and which inputs they’ll be cutting back on most in 2011. Like most years, growers say energy is their most burdensome input. Pots and trays, followed by soil and amendments, chemicals and fertilizers, are the next-most burdensome inputs. Labels and tags and irrigation are the two areas the majority of growers seem to be handling all right.

To dig deeper on inputs, we asked growers which of the following inputs they will cut back on most in 2011. Energy was the most popular response, although only half of the growers who indicate energy is their biggest input burden say they will cut back. It’s an input growers absolutely can’t do without, after all, and before many begin cutting back and turning toward an alternative system, a substantial upfront investment must be made.

Behind energy, growers indicate chemicals and pots and trays are the areas in which they’ll be cutting back most.

What They’re All Saying

Part of our annual State Of The Industry survey was constructed with open-ended questions to generate more feedback and extract more specific information from growers and suppliers. For example, we asked growers about the biggest challenges the industry needs to address in order to collectively move growers into growth positions. Here’s what a few had to say:

• “Housing, housing, housing. Until we start building again, sales will struggle.” – Steve Larson, BASF

• “We need to find a product or product mix that appeals to the young consumer. They are our future big spenders. They are not looking to own their own homes like the (Baby) Boomers. This could lead to shrinking markets. – Kevin Wilson, Shademakers Nursery & Landscape

• “Growth in flowers will be difficult. What we experienced in 2010 will probably be the same in 2011. Growing food products in the fall and winter months may be an answer. Locally grown is more than a trend; it is a marketing concept that is going to grow in demand. We have to find ways to cash in on these new developments.” – Ron Eberly, American Clay Works & Supply Co.

• “Pricing is a major issue on all agricultural items, not just greenhouse crops. Everyone needs to stop lowering prices. Has there been any real gain in this area since the 1980s? We must all learn to market the products and entice more demand.” – Brian Kanotz, Callaway Gardens

• “Jobs need to recover but relevance for ornamental horticulture also needs to increase. Competition for discretionary dollars is growing.” – Kurt Parbst, Ludvig Svensson

• “Pricing that correlates to a quality product with excellent support and service behind every sale is a must.” – Scott Thompson, X.S. Smith

Subscribe to eNewsletter