Greenhouse Grower’s 2026 Top 100 Growers: The Complete List

May 24, 2026

May 24, 2026

Greenhouse Grower’s annual Top 100 Growers ranking, which you can find at the bottom of this page, tracks the nation’s largest floriculture operations by square footage of production. The 2026 list, compiled through an online survey and frequent communication with the growers on the list, reflects an industry that looks a little different than it did just a year ago. Size still matters, of course. But this year’s Top 100 is about more than square footage alone. The survey points to how the industry’s largest growers are responding to slower expansion, ongoing labor and cost pressure, consolidation, and the need to operate more efficiently. This year’s list is not just a ranking. It is a look at how the biggest growers are adjusting to a new phase of growth.

Less Expansion, More Efficiency

From 2025 to 2026, the Top 100 growers added a combined 428,000 square feet of production. That figure, however, is heavily influenced by one major change: Metrolina Greenhouses added 1.4 million square feet through its merger with South Central Growers in Tennessee. Without that addition, the Top 100 would have posted a net decline of 970,000 square feet.

That shift aligns with what some growers described in this year’s survey. After a period of expansion, many operations are focusing more closely on using existing space efficiently. As one grower put it, “We grew a lot over the last couple of years, and now we’re focused on becoming more efficient with the space we have.”

The list itself supports that change — 22 companies grew in size this year, 13 got smaller, and 65 reported no change from 2025. A year ago, 25 companies expanded, and the Top 100 posted more than 1.5 million square feet of combined growth. This year’s numbers point to a different phase for the industry’s largest growers, one defined less by expansion and more by discipline, efficiency, and getting more out of the space already in place.

Consolidation Continues

The biggest Top 100 development of the past year was the merger between Metrolina Greenhouses in North Carolina and South Central Growers in Tennessee. The combined organization now operates under the Metrolina Greenhouses brand, adding significant square footage while expanding the company’s geographic reach and retail capacity.

Other ownership changes also stood out. N.G. Heimos Greenhouses, Smith Gardens, and American Farms are now under the ownership of the Hoffmann Family of Companies, though each continues to operate under its existing brand. Four Star Greenhouses and Pleasant View Gardens are also now official Proven Winners companies and remain listed separately under that umbrella.

Consolidation remains a defining part of how the Top 100 is evolving. Large operations are not only adjusting internally. In some cases, they are becoming part of bigger platforms with broader reach, deeper resources, and stronger alignment across production, branding, and retail relationships.

One notable difference from a year ago is that none of the companies on the 2025 Top 100 list dropped off because of closure. In a period when ownership shifts and strategic mergers are still reshaping the industry, that stability stands out.

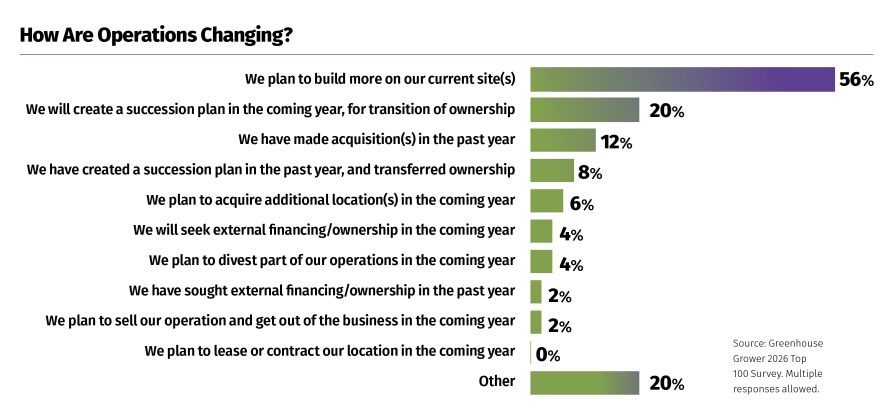

How Are Operations Changing?

Adjusting to Evolving Market Conditions

The past few years have brought both opportunity and strain for floriculture. Consumer interest in plants remains positive, but that momentum has not insulated growers from higher costs, shifting customer demand, labor pressure, and other market challenges. Some long-standing operations have closed in recent years. Others have responded by becoming more focused, more efficient, or more flexible.

That mindset came through clearly in the survey responses. Growers pointed to a range of adjustments that helped them stay competitive, from bringing more propagation in-house and refining product mix to building better control over transportation, labor, and overhead. Some narrowed their focus to core business areas. Others looked for efficiency gains in small but meaningful ways. Still others responded by shifting sales strategy, strengthening partner relationships, or staying nimbler as market conditions changed.

As one grower noted, “We built our own truck fleet for better control around transportation costs. We’re also participating in the H-2A program and investing in automation for better control around labor shortages.” Another said the company “focused on our core business of growing young plants for other growers while selling finished annuals to just one retailer.” Others described moving production into slightly smaller pot and input sizes to reduce overhead, doing more propagation in-house to offset raw material costs, or refocusing sales into new channels as customer demand shifted.

The approaches differ, but the larger lesson is the same. The growers weathering change most effectively are not relying on one solution. They are making practical adjustments across transportation, labor, production, sales, and customer relationships to stay resilient in a more demanding market.

An Eye on the Future

For all the pressure growers are managing, the outlook in floriculture is not defined by caution alone. The survey responses also showed a strong sense of optimism about where the industry is headed, especially around new genetics, automation, leadership development, and the long-term staying power of plants themselves.

Some growers pointed to innovation as the biggest reason for confidence. They are excited about new perennial genetics, the continued evolution of automation, and the opportunity to keep developing products that appeal to both new and existing consumers. Others see promise in technologies beginning to reshape how greenhouse businesses operate, from artificial intelligence and predictive analytics to e-commerce and drone technology. In several responses, growers made it clear that fresh ideas and new tools are becoming part of how the next phase of growth will happen.

That optimism is not only about technology. It is also about people. Several respondents said they are encouraged by the next generation coming into the industry, whether that means children returning to the family business, younger leaders bringing a different perspective, or stronger involvement in youth and education programs that help build future horticulture talent. Others pointed to continued demand for high-quality plants and the enduring consumer connection to gardening as reasons to stay bullish about the years ahead.

Even with tighter margins, consolidation, and a more disciplined operating environment, many of the industry’s largest growers still see meaningful room for innovation, leadership renewal, and long-term demand. The challenges are real, but so is the sense that floriculture still has room to grow.

| 2026 Rank | 2025 Rank | Name Of Operation | State | 2026 Total (Environmentally Controlled Square Feet) |

|---|---|---|---|---|

| 1 | 1 | Costa Farms | FL | 46,739,880 |

| 2 | 2 | Altman Plants | CA | 38,480,855 |

| 3 | 3 | Bell Nursery | MD | 18,150,000 |

| 4 | 4 | Bonnie Plants* | AL | 15,908,587 |

| 5 | 5 | Metrolina Greenhouses | NC | 10,800,000 |

| 6 | 6 | Kurt Weiss Greenhouses* | NY | 9,238,232 |

| 7 | 7 | Rocket Farms* | CA | 7,500,000 |

| 8 | 8 | Green Circle Growers | OH | 6,795,360 |

| 9 | 9 | Woodburn Nursery and Azaleas | OR | 5,052,960 |

| 10 | 10 | Olson's Greenhouse Gardens | UT | 5,035,440 |

| 11 | 12 | Smith Gardens | WA | 4,100,000 |

| 12 | 11 | Dan and Jerry's Greenhouses | MN | 4,076,345 |

| 13 | 13 | Coastal Greenhouses* | NY | 3,746,160 |

| 14 | 14 | Speedling | FL | 3,417,000 |

| 15 | 23 | Hoffmann Heimos Greenhouses LLC | IL | 2,985,300 |

| 16 | 15t | Dallas Johnson Greenhouses | IA | 2,831,400 |

| 17 | 15t | Wenke/Sunbelt Greenhouses | MI | 2,781,825 |

| 18 | 19 | Dewar Nurseries | FL | 2,684,800 |

| 19 | 18 | Bergen's Greenhouses Inc. | MN | 2,592,937 |

| 20 | 20 | Young's Plant Farm | AL | 2,447,300 |

| 21 | 21 | Matsui Nursery | CA | 2,400,000 |

| 22 | 22 | Natural Beauty Growers | WI | 2,381,000 |

| 23 | 17 | Headstart Nursery | CA | 2,200,000 |

| 24 | 25 | Plug Connection LLC | CA | 2,061,000 |

| 25 | 26 | Lucas Greenhouses | NJ | 2,046,636 |

| 26 | 24 | Grower Direct Farms | CT | 2,018,000 |

| 27 | 27 | Aris Horticulture | OH | 2,007,800 |

| 28 | 28 | Garden State Growers | NJ | 2,003,760 |

| 29 | 29t | Milgro Nursery | UT | 2,000,000 |

| 30 | 31 | Armstrong Growers/Pike Farm | CA | 1,945,000 |

| 31 | 33 | Bailey Nurseries | MN | 1,776,554 |

| 32 | 34 | Westland Floral Co.* | CA | 1,740,000 |

| 33 | 35 | Pineae Greenhouses | UT | 1,710,240 |

| 34 | 36 | Willoway Nurseries, Inc. | OH | 1,664,800 |

| 35 | 38 | Henry Mast Greenhouses | MI | 1,591,127 |

| 36 | 32 | Rockwell Farms | NC | 1,568,160 |

| 37t | 40 | Corso's Horticulture | OH | 1,500,000 |

| 37t | 39 | Kawahara Nurseries | CA | 1,500,000 |

| 39 | 41 | American Color | VA | 1,393,920 |

| 40 | 42 | Silver Vase | FL | 1,322,000 |

| 41 | 43 | Plainview Growers | NJ | 1,316,400 |

| 42 | 37 | Post Gardens | MI | 1,306,800 |

| 43 | 44 | Richardson Bros Greenhouses | IL | 1,300,000 |

| 44 | 45 | Quality Greenhouses and Perennial Farm | PA | 1,239,000 |

| 45 | 50 | Green Valley Greenhouse | MN | 1,227,372 |

| 46 | 46 | Heartland Growers | IN | 1,226,682 |

| 47 | 49 | Red Oak Greenhouses, Inc. | IA | 1,219,680 |

| 48 | 52 | Masson Farms of New Mexico | NM | 1,141,141 |

| 49 | 56 | Proven Winners Carleton (formerly Four Star Greenhouses) | MI | 1,132,560 |

| 50 | 51 | Van Wingerden International, Inc. | NC | 1,102,104 |

| 51 | 29t | Tagawa Greenhouses | CO | 1,100,000 |

| 52t | 52t | Catoctin Mountain Growers | MD | 1,089,000 |

| 52t | n/a | Heart of Florida Greenhouses | FL | 1,089,000 |

| 52t | 52t | Nash Greenhouses | MI | 1,089,000 |

| 55 | 54 | Bob's Market & Greenhouses, Inc. | WV | 1,080,000 |

| 56 | n/a | Color Orchids | TX | 1,032,000 |

| 57 | 79t | Plants Unlimited Inc. | FL | 1,020,000 |

| 58 | 61 | McCorkle Nurseries* | GA | 980,000 |

| 59 | 61 | Kube-Pak | NJ | 933,000 |

| 60 | 59 | van Hoekelen Greenhouses, Inc. | PA | 916,000 |

| 61 | 60 | Countryside Greenhouses* | MI | 914,760 |

| 62 | 47 | Deroose Plants Inc. | FL | 900,000 |

| 63 | 62 | Petitti/Casa Verde Growers | OH | 895,000 |

| 64 | 63 | Myriad Flowers International | CA | 871,200 |

| 65 | 64 | Sedan Floral, Inc. | KS | 852,135 |

| 66t | 65t | Baucom's Nursery | NC | 850,000 |

| 66t | 65t | Fessler Nursery | OR | 850,000 |

| 68 | 67 | Kent's Bromeliad Nursery | CA | 840,000 |

| 69 | 68 | Botany Lane Greenhouses | CA | 827,640 |

| 70 | 69 | Andy Mast Greenhouses | MI | 826,921 |

| 71 | 72 | Dutch Heritage Gardens | CO | 825,000 |

| 72 | 70 | Dickman Farms | NY | 815,000 |

| 73 | 73 | Walters Gardens | MI | 775,368 |

| 74 | 57 | Proven Winners Loudon (formerly Pleasant View Gardens) | NH | 772,096 |

| 75t | 74t | California Pajarosa | CA | 760,000 |

| 75t | 74t | Olive Hill Greenhouses | CA | 760,000 |

| 77 | 76 | Premier Growers | GA | 750,000 |

| 78 | 81 | Esbenshades Greenhouses | PA | 744,960 |

| 79 | 77 | Naturally Beautiful Plant Products | NJ | 732,700 |

| 80 | 83 | N. Casertano Greenhouses and Farms | CT | 710,028 |

| 81 | 78 | Agromillora | CA | 700,880 |

| 82 | 79t | Knox Nursery | FL | 700,000 |

| 83 | 95 | New Leaf Growers | PA | 681,480 |

| 84 | 82 | Darrell Norris & Son Greenhouses | OH | 681,216 |

| 85 | n/a | Hampshire Farms LLC | IL | 664,140 |

| 86 | 84 | Parks Brothers Farm | AR | 660,000 |

| 87 | 85t | American Farms | FL | 655,000 |

| 88t | 85t | Green Valley Floral | CA | 653,400 |

| 88t | 92t | Van Wingerden Greenhouses, Inc. | WA | 653,400 |

| 88t | 85t | Vera's Nursery* | FL | 653,400 |

| 91 | 89 | Micandy Gardens Greenhouses | MI | 645,000 |

| 92 | 90 | Pleasant Valley Farms | AR | 644,056 |

| 93t | 92t | Guthrie Greenhouses | OK | 609,840 |

| 93t | 91 | Tidal Creek Growers | MD | 609,840 |

| 95t | n/a | Neosho Gardens | KS | 600,000 |

| 95t | 71 | Westerlay Orchids | CA | 600,000 |

| 97 | 96 | Roseville Farms | FL | 560,000 |

| 98 | 97 | Emerald Coast Growers | FL | 540,000 |

| 99t | 99t | Plants In Design, Inc.* | FL | 522,000 |

| 99t | 99t | T&L Nursery | WA | 522,000 |

| t = tie | n/a = not ranked | * = estimated |

Subscribe to eNewsletter