The Latest PPP Loan Forgiveness Guidance for Greenhouse Growers

May 24, 2020

May 24, 2020 Since the passage of the CARES Act in late March, there have been several changes, clarifications, updates, and other moving parts related to applying for funding through the Paycheck Protection Program (PPP). Most recently, the updates have focused on loan forgiveness and tax implications.

As always, AmericanHort and its partner organization K-Coe Isom have been on top of these changes. The two of them hosted a webinar that featured several insights and suggestions on what growers who have applied, or are still considering applying, need to know.

The full webinar is available for on-demand viewing here. Here are some of the highlights, mostly presented by K-Coe Isom advisors Kala Jenkins and Beth Swanson.

- As of May 20, $513 billion in loans through the PPP had been approved, leaving nearly $145 billion still available. There were initial concerns that the available funds would be quickly depleted, but with that not being the case, lenders have had more time to thoroughly review applications.

- At the same time, there has been more guidance when it comes to how seasonal workers should be factored into payroll numbers. Long story short, it was just two weeks ago that seasonal employers were limited in how they could alter the time period they used to calculate payroll periods. Now, with the Small Business Administration (SBA) recognizing that seasonal employers have different calendars, there are more opportunities. Employers can now pick any 12-week window between May 1-Sept. 15, 2019. If you’ve already applied, and your lender has not yet submitted form 1502 of the application, you can go back and ask for additional funding if choosing a new 12-week period might be better for you.

- The webinar included several updates on safe harbor provisions. For example, the SBA has noted that if your loan request was for less than $2 million, you are safe from any audit process. However, those who applied for more than $2 million in loans can be pulled for an audit, which would require documentation on financial hardships you are facing, or other circumstances. Perhaps the biggest takeaway is this: Documentation will be critical when applying for forgivable loans, so document every step of the process you can.

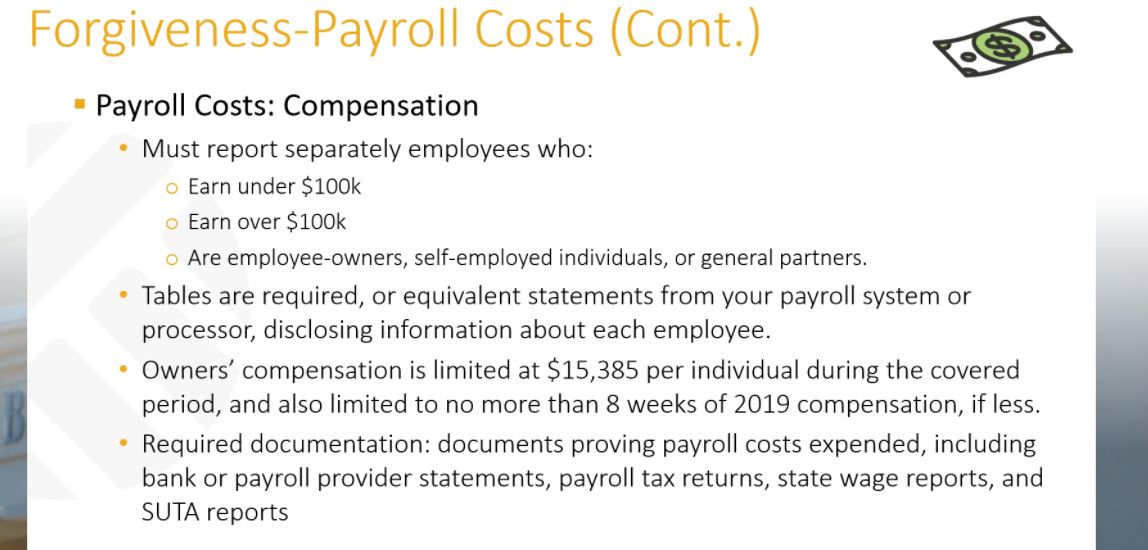

- The SBA can perform an audit up to six years after you turn in your forgiveness application. So, make sure you keep all documentation (good faith certification) on file for six years in case you are audited. The image below goes into more detail on payroll documentation.

- The ability to use PPP loans beyond payroll continues to be a key talking point. Mortgage, rent, and utility costs are mostly allowable, but there is no clarification on transportation costs. Your best approach: track these costs and stay tuned.

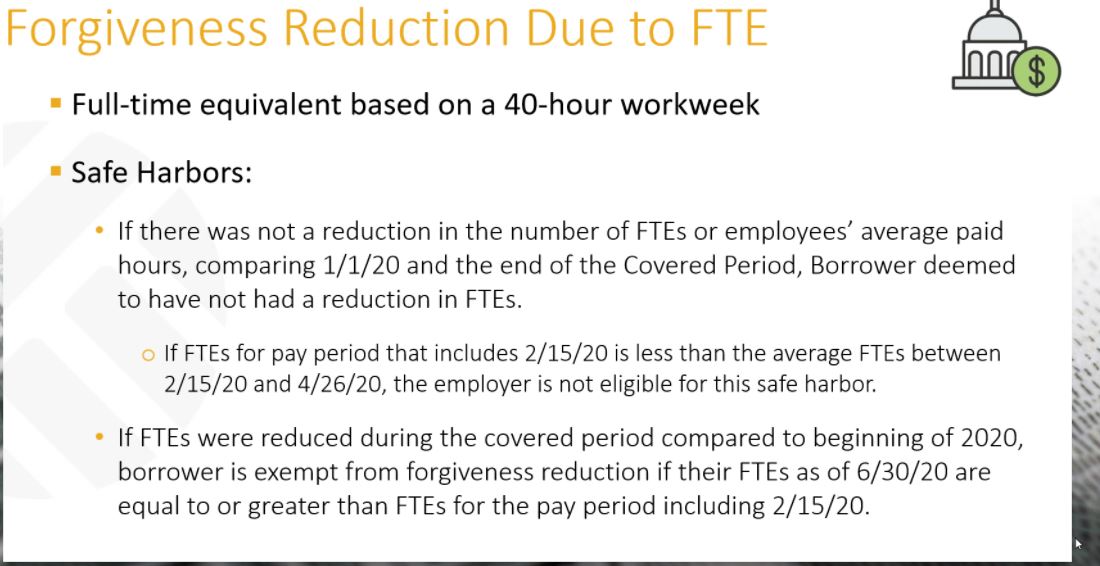

- Safe harbor protections concerning full-time employee (FTE) calculations continue to be updated. See the image below for details.

- There is a three-step process to determine a potential reduction in forgiveness due to reductions in employee compensation (if you had to furlough employees). This must be calculated for each employee earning less than $100,000. Step 1: Determine if the employee’s pay was reduced by more than 25%; Step 2: Determine if the Safe Harbor test is met (if the employee’s pay is restored by June 30, no forgiveness reduction applies); Step 3: Determine the wage reduction (computed based on average pay for hourly employees, and based on annualized salaries for salaried employees)

- Need clarification on how to handle H-2A employees? AmericanHort has posted a one-page guidance on this topic on its Coronavirus Resource Center website.

- Finally, AmericanHort is in the process of developing a whitepaper that compiles data on how the horticulture industry is taking advantage of the Paycheck Protection Program, with the goal of helping you plan for the necessary documentation

0

1

5

The Latest PPP Loan Forgiveness Guidance for Greenhouse Growers

Subscribe to eNewsletter